The

MacroEconomic Calendar

The MacroEconomic Calendar

Apr 7, 2025

Week of April 7, 2025

Week of April 7, 2025

AJ Giannone, CFA

The Setup & Where to Focus

Stocks plunged post Liberation Day, with the S&P 500 losing 9.1% for its worst week since March 2020. It was a global selloff by week’s end, and few corners of the market were left unscathed.

The Nasdaq Composite tumbled 10%, finishing on the week's lows, with the Magnificent Seven stocks collectively in a drawdown close to 30%. Former stalwarts such as Apple (AAPL), NVIDIA (NVDA), and Meta Platforms (META) each plummeted more than 15%.

Ahead of earnings season, Financials like JPMorgan Chase (JPM), Goldman Sachs (GS), Bank of America (BAC), and Wells Fargo (WFC) collapsed 15-19%. While defensives sectors outperformed, they, too, were taken to the woodshed by Friday afternoon.

The Cboe Volatility Index (VIX) soared to 45 and hovered there throughout much of Friday’s session.

A 45 VIX implies a daily swing in the S&P 500 of 3%, but action in the days ahead may be even more volatile.

The Cboe 1-day VIX product settled Friday above 80, implying a staggering 5.2% SPX change on Monday. Of course, the S&P 500 fell by 4.9% on Thursday and 5.9% last Friday.

The macro data took a backseat to Wednesday afternoon’s Liberation Day tariff announcement from the White House Rose Garden.

Stocks initially lifted that evening when President Trump discussed universal tariffs, but once he brought out the now-infamous posterboard chart of reciprocal tariff rates, the bears were off to the races.

Import duties are set to be as high as 49%. The EU’s additional rate is listed at 20%, and China’s is 34% (which brings its total percentage to 54%, and some argue the effective rate is even higher).

Revenue is expected to be collected starting Wednesday this week, but that all depends on the POTUS.

It’s possible that countries and blocs, big and small, convened over the weekend after the global stock market rout to hash out deals with the US. Another thought is that the proposed US tariffs are so high that there may be adjustments to them, or they might not be in place for very long.

Still, President Trump was firm, reinforcing their permanence. It will be a fluid situation in the days ahead, with global investors on edge.

We continue to believe this will ultimately be a good development. The president and Treasury Secretary Bessent have said all along that there will be an adjustment period—a euphemism for financial market pain.

Once trade policy firms up and the US is treated fairly by both our allies and adversaries, the policy focus can shift to the bullish stuff—tax cuts and deregulation.

By then, interest rates may be lower, and the private sector—not the federal government—will be the engine of job growth. It’s also important to highlight that the market’s leaders—the Mag 7—were due for a protracted pullback.

As of Friday’s close, the S&P 500 traded under 19x forward earnings estimates, with the Mag 7 sporting a mid-20s price-to-earnings ratio, down from above 30x.

Overlooked on Friday was a strong jobs report.

The economy added 228,000 positions, sharply above the consensus forecast of 140,000. Though January and February’s payroll gains were modestly revised lower, private payrolls grew by 209,000 last month, also better than expected.

The unemployment rate inched up from 4.139% to 4.152%--essentially unchanged from February and within the range since last summer.

The household survey, used to calculate the unemployment rate, also showed a 200,000+ jobs climb. Average hourly earnings ticked down to 3.8%, helping the inflation situation, and weekly hours worked was steady at 34.2.

The sanguine data in the BLS report included a slight increase in the labor force participation rate and a surprisingly large jump in the number of full-time workers.

What was not as bullish was the mix of positions—heavy in non-cyclical education & health services.

The healthy March employment survey came after sanguine Initial Jobless Claims data but a fresh cycle high in Continuing Claims.

Last month’s Challenger, Gray, and Christmas job cuts number was massive, but it was driven mainly by government layoffs—which we are fine with seeing.

ADP Private Payrolls for March, like the government’s Nonfarm Payrolls report, was above estimates.

On net, the labor market continues to hang in there, but that could all change in the months ahead.

According to online betting markets, there’s now a more than 60% chance of recession this year—Q1 US real GDP growth is expected to have stalled at just +0.1%.

Elsewhere last week, PMI survey numbers verified close to estimates, with the S&P Global Manufacturing PMI creeping back above 50 (50.2) and the ISM’s version falling below 50 (49.0). Services PMIs are now 54.4 and 50.8, respectively. Construction Spending rose more than forecast, as did Durable Goods Orders for February. Last week’s body of macro data suggests the US economy grew but was very much in wait-and-see mode, too.

It's easy to get lost in the onslaught of macro narratives, but price action can help tell the tale.

Not surprisingly, the best sectors were Consumer Staples (XLP), Utilities (XLU), Real Estate (XLRE), and Health Care (XLV) last week. Those defensive niches were all down, however.

The worst sectors were Industrials (XLI), Financials (XLF), Information Technology (XLK), and Energy (XLE). Oil & gas stocks were obliterated on Thursday and Friday, shedding more than 16%, as WTI cratered into the low $60s—a weekly closing settle not seen since April 2021.

Semiconductors (SMH) was another corner the bears ravaged—it likewise crashed 16%, erasing chip stocks’ gains going back to early 2024.

Interestingly, homebuilders (ITB) and retail (XRT) outperformed for the week, perhaps due to the fall in interest rates and some positive headlines that tariffs between the US and Vietnam will be lifted.

Weekly losses of 8-10% across the board were seen. US large and small caps moved in lockstep, and international equities, which had been outperforming, were slammed on Friday.

The Vanguard Total Stock Market ETF (VTI) lost 9.1%, and the Vanguard FTSE All-World ex-US ETF (VEU) took an 8.1% hit.

Mexico (EWW) outperformed, down a mere 3.3%, but the year’s top-performing country ETF—Poland (EPOL)--was punished, -12%.

There were big moves in bonds, as well.

The yield on the benchmark 10-year Treasury note was 4.4% as of March 27. By Friday, April 4, it touched 3.86% as an intense and classic safety trade was on. As happens during panics, correlations eventually gravitated toward one, and Treasuries were sold Friday afternoon.

The 10-year yield closed the week at 4.00%, still roughly 0.4 percentage points above last September’s nadir.

Junk bonds suffered sharply—yet another recessionary signal. The 2-year Treasury yield was under 3.5% for a time, but it rose 17 basis points off its low to close at 3.64%.

Part of the bond selling was pinned to somewhat hawkish comments from Fed Chair Powell around lunchtime Friday—he took back his stance that tariff-induced inflation was likely to be transitory, noting that it would take some time to determine the right policy action.

As it stands, traders price in a 1-in-3 chance of a May cut. Four to five quarter-point eases are discounted into the December Fed Funds futures contract.

The US Dollar Index sank through Thursday but rallied sharply on Friday.

Finally, turning to commodities, we highlighted oil’s puke, but gold and silver suffered by week’s end, too.

We mentioned in March that the gold market is prone to intense selloffs that come with little warning, and that certainly played out to close the week. Spot gold backed down from $3163 to $3016 per ounce, posting just its second negative week of 2025.

Amid all the wild price action—declines not seen since COVID, major technical areas breached, and intense selling across asset classes—bitcoin was up. Not only was it higher, but price action was downright dull in the world’s biggest cryptocurrency. It was steady in the mid-$80,000s. That’s something to watch—if macro pressures ease, crypto could be like a submerged beach ball ready to resurface.

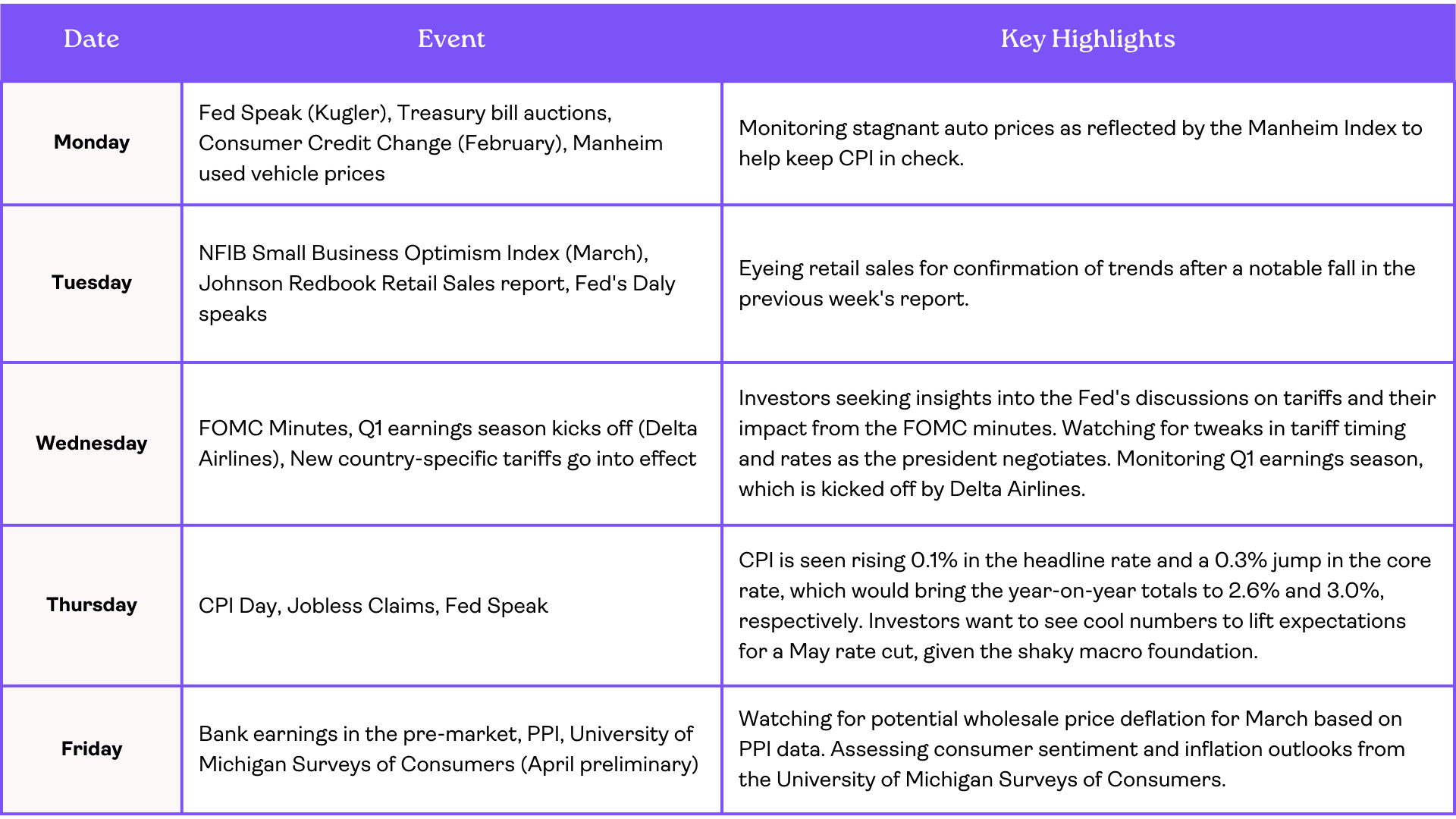

Weekly Calendar Look Ahead

With intense volatility expected this week, macro data points may not have the impact they usually do. Still, a host of inflation data points are on tap after last week’s generally decent employment updates.

Monday is quiet with Fed speak from Kugler (a dove) Monday morning with Treasury bill auctions thereafter.

February’s Consumer Credit Change hits in the afternoon, and we’ll get the final update on Manheim used vehicle prices.

The Manheim Index has been encouraging lately, pointing to stagnant auto prices, which, along with the crash in eggs, should help keep CPI in check.

Tuesday’s primary catalyst will be the March NFIB Small Business Optimism Index’s release.

It has been the holdout vibes gauge that remains above average, but small-business fervor cooled sharply in January and February after printing a multi-year high after President Trump’s November win.

It leans Republican, so this could be a decent barometer of how much pressure may be put on Trump to reverse his stern trade policy.

We’ll also get the weekly Johnson Redbook Retail Sales report—it fell notably last week, so our team will monitor it for confirmation on Tuesday morning.

The Fed’s Daly (a dove) speaks in the afternoon.

Wednesday’s key macro catalyst is the FOMC Minutes, which publishes at 2 p.m. ET.

Investors will be curious to read what the voting members discussed at the March Fed meeting and how much tariffs played into their dots.

Before the bell, Delta Airlines (DAL) kicks off the Q1 earnings season, with the big banks reporting Friday morning.

Wednesday is also when the new country-specific tariffs go into effect, but we think there will be tweaks in the timing and rates as the president negotiates.

Thursday is CPI Day.

The consensus calls for a 0.1% rise in the headline rate and a 0.3% jump in the core rate. That would bring the year-on-year totals to 2.6% and 3.0%, respectively.

Cool numbers would lift expectations for a May cut, and investors want to see that now, given the shaky macro foundation.

Jobless Claims and Fed speak come in the morning, too.

Friday’s focus will be on bank earnings in the pre-market, but PPI then takes the spotlight.

We could actually see some wholesale price deflation for March—something to keep an eye on.

The first full week of the second quarter wraps up with the April preliminary University of Michigan Surveys of Consumers, which is widely expected to show dreadful sentiment readings and high inflation outlooks.

In reality, the US 10-year breakeven inflation rate has cratered to 2.18% on the back of the oil price plunge—the lowest since last September.

Fiscal Policy Framework

Effective April 5, a universal 10% tariff applied to all imports, with higher reciprocal rates targeting specific counties starting April 9. With extremely high levies on Chinese goods and auto imports, the near-term aim is to raise revenue to fund later tax cuts. International tensions will be high, but nations will likely reach out to President Trump to reduce overall tariff rates.

Our team is also on watch for a global coordinated effort to appease Trump, which could introduce true free trade sooner than what so many pessimists expect. Countermeasures from China could be the first of several near-term retaliatory tariffs, but other nations just don’t hold the leverage—a protracted period of high tariffs poses depression-like risks to countries dependent upon exports.

It’s also possible that President Trump will offer tax credits and exemptions to US companies that have played by the rules by shifting production out of China in the past decade. We believe it’s important to call out that Trump said, “The markets are going to boom,” while aboard Air Force One late last week, so a Trump put may still exist.

Meanwhile, Senate Republicans push forward with a budget resolution to tap the reconciliation process for tax and spending legislation; the GOP must extend Trump’s 2017 tax cuts.

Last week, special elections in Florida went in the Republicans’ favor, and it’s too early to take them and the Wisconsin Supreme Court race as 2026 bellwethers. What will be important, though, is any potential GOP Trump defection with the midterms 19 months away. With no third term expected, it will be challenging for RINO Republicans to exert forceful political pressure on the POTUS.

Risks & Opportunities

S&P 500 earnings estimates are very likely to be further trimmed with odds of recession ticking above 60%; that’s a negative headline risk in the weeks ahead

Corporate executives may likewise voice a cautionary tone in the upcoming earnings season, potentially resulting in backlash from Trump

We expect extremely downbeat sentiment numbers this week, but that may present an opportunity to add on risk from a contrarian perspective

Weak inflation numbers on Thursday and Friday would increase rate-cut chances, and a Fed put could come sooner than later

A drop below 5000 on the S&P 500 could quickly lead to a test of the 4918 –20% psychological bear-market level

Quick Hits

The S&P 500 lost 10.5% between Thursday and Friday; 2-day declines of that magnitude were only seen in October 1987, November 2008, and March 2020 (since 1980)

The SPX is off to its 6th worst start to a year since 1950 (-13.7%); in comparable years, returns were strong for the balance of the year

The average US large-cap stock is down 20.3% YTD

The S&P 500 closed below its 38.2% Fibonacci retracement level of 5133, with the –20% bear market threshold at 4918, 3% below Friday’s settle

US and European large caps typically fall 30-35% during recessions

The VIX settled above 45 for the week—only seen before in October 2008-March 2009 and March 2020

The Nasdaq Composite is now below where it traded in November 2021, the Russell 2000 is within earshot of its August 2018 high, and international stocks are below prices from June 2021

The Cboe reported record put option trading volume on Thursday and Friday; record NYSE volume occurred Friday

Mortgage rates declined to a six-month low at 6.55%

The Setup & Where to Focus

Stocks plunged post Liberation Day, with the S&P 500 losing 9.1% for its worst week since March 2020. It was a global selloff by week’s end, and few corners of the market were left unscathed.

The Nasdaq Composite tumbled 10%, finishing on the week's lows, with the Magnificent Seven stocks collectively in a drawdown close to 30%. Former stalwarts such as Apple (AAPL), NVIDIA (NVDA), and Meta Platforms (META) each plummeted more than 15%.

Ahead of earnings season, Financials like JPMorgan Chase (JPM), Goldman Sachs (GS), Bank of America (BAC), and Wells Fargo (WFC) collapsed 15-19%. While defensives sectors outperformed, they, too, were taken to the woodshed by Friday afternoon.

The Cboe Volatility Index (VIX) soared to 45 and hovered there throughout much of Friday’s session.

A 45 VIX implies a daily swing in the S&P 500 of 3%, but action in the days ahead may be even more volatile.

The Cboe 1-day VIX product settled Friday above 80, implying a staggering 5.2% SPX change on Monday. Of course, the S&P 500 fell by 4.9% on Thursday and 5.9% last Friday.

The macro data took a backseat to Wednesday afternoon’s Liberation Day tariff announcement from the White House Rose Garden.

Stocks initially lifted that evening when President Trump discussed universal tariffs, but once he brought out the now-infamous posterboard chart of reciprocal tariff rates, the bears were off to the races.

Import duties are set to be as high as 49%. The EU’s additional rate is listed at 20%, and China’s is 34% (which brings its total percentage to 54%, and some argue the effective rate is even higher).

Revenue is expected to be collected starting Wednesday this week, but that all depends on the POTUS.

It’s possible that countries and blocs, big and small, convened over the weekend after the global stock market rout to hash out deals with the US. Another thought is that the proposed US tariffs are so high that there may be adjustments to them, or they might not be in place for very long.

Still, President Trump was firm, reinforcing their permanence. It will be a fluid situation in the days ahead, with global investors on edge.

We continue to believe this will ultimately be a good development. The president and Treasury Secretary Bessent have said all along that there will be an adjustment period—a euphemism for financial market pain.

Once trade policy firms up and the US is treated fairly by both our allies and adversaries, the policy focus can shift to the bullish stuff—tax cuts and deregulation.

By then, interest rates may be lower, and the private sector—not the federal government—will be the engine of job growth. It’s also important to highlight that the market’s leaders—the Mag 7—were due for a protracted pullback.

As of Friday’s close, the S&P 500 traded under 19x forward earnings estimates, with the Mag 7 sporting a mid-20s price-to-earnings ratio, down from above 30x.

Overlooked on Friday was a strong jobs report.

The economy added 228,000 positions, sharply above the consensus forecast of 140,000. Though January and February’s payroll gains were modestly revised lower, private payrolls grew by 209,000 last month, also better than expected.

The unemployment rate inched up from 4.139% to 4.152%--essentially unchanged from February and within the range since last summer.

The household survey, used to calculate the unemployment rate, also showed a 200,000+ jobs climb. Average hourly earnings ticked down to 3.8%, helping the inflation situation, and weekly hours worked was steady at 34.2.

The sanguine data in the BLS report included a slight increase in the labor force participation rate and a surprisingly large jump in the number of full-time workers.

What was not as bullish was the mix of positions—heavy in non-cyclical education & health services.

The healthy March employment survey came after sanguine Initial Jobless Claims data but a fresh cycle high in Continuing Claims.

Last month’s Challenger, Gray, and Christmas job cuts number was massive, but it was driven mainly by government layoffs—which we are fine with seeing.

ADP Private Payrolls for March, like the government’s Nonfarm Payrolls report, was above estimates.

On net, the labor market continues to hang in there, but that could all change in the months ahead.

According to online betting markets, there’s now a more than 60% chance of recession this year—Q1 US real GDP growth is expected to have stalled at just +0.1%.

Elsewhere last week, PMI survey numbers verified close to estimates, with the S&P Global Manufacturing PMI creeping back above 50 (50.2) and the ISM’s version falling below 50 (49.0). Services PMIs are now 54.4 and 50.8, respectively. Construction Spending rose more than forecast, as did Durable Goods Orders for February. Last week’s body of macro data suggests the US economy grew but was very much in wait-and-see mode, too.

It's easy to get lost in the onslaught of macro narratives, but price action can help tell the tale.

Not surprisingly, the best sectors were Consumer Staples (XLP), Utilities (XLU), Real Estate (XLRE), and Health Care (XLV) last week. Those defensive niches were all down, however.

The worst sectors were Industrials (XLI), Financials (XLF), Information Technology (XLK), and Energy (XLE). Oil & gas stocks were obliterated on Thursday and Friday, shedding more than 16%, as WTI cratered into the low $60s—a weekly closing settle not seen since April 2021.

Semiconductors (SMH) was another corner the bears ravaged—it likewise crashed 16%, erasing chip stocks’ gains going back to early 2024.

Interestingly, homebuilders (ITB) and retail (XRT) outperformed for the week, perhaps due to the fall in interest rates and some positive headlines that tariffs between the US and Vietnam will be lifted.

Weekly losses of 8-10% across the board were seen. US large and small caps moved in lockstep, and international equities, which had been outperforming, were slammed on Friday.

The Vanguard Total Stock Market ETF (VTI) lost 9.1%, and the Vanguard FTSE All-World ex-US ETF (VEU) took an 8.1% hit.

Mexico (EWW) outperformed, down a mere 3.3%, but the year’s top-performing country ETF—Poland (EPOL)--was punished, -12%.

There were big moves in bonds, as well.

The yield on the benchmark 10-year Treasury note was 4.4% as of March 27. By Friday, April 4, it touched 3.86% as an intense and classic safety trade was on. As happens during panics, correlations eventually gravitated toward one, and Treasuries were sold Friday afternoon.

The 10-year yield closed the week at 4.00%, still roughly 0.4 percentage points above last September’s nadir.

Junk bonds suffered sharply—yet another recessionary signal. The 2-year Treasury yield was under 3.5% for a time, but it rose 17 basis points off its low to close at 3.64%.

Part of the bond selling was pinned to somewhat hawkish comments from Fed Chair Powell around lunchtime Friday—he took back his stance that tariff-induced inflation was likely to be transitory, noting that it would take some time to determine the right policy action.

As it stands, traders price in a 1-in-3 chance of a May cut. Four to five quarter-point eases are discounted into the December Fed Funds futures contract.

The US Dollar Index sank through Thursday but rallied sharply on Friday.

Finally, turning to commodities, we highlighted oil’s puke, but gold and silver suffered by week’s end, too.

We mentioned in March that the gold market is prone to intense selloffs that come with little warning, and that certainly played out to close the week. Spot gold backed down from $3163 to $3016 per ounce, posting just its second negative week of 2025.

Amid all the wild price action—declines not seen since COVID, major technical areas breached, and intense selling across asset classes—bitcoin was up. Not only was it higher, but price action was downright dull in the world’s biggest cryptocurrency. It was steady in the mid-$80,000s. That’s something to watch—if macro pressures ease, crypto could be like a submerged beach ball ready to resurface.

Weekly Calendar Look Ahead

With intense volatility expected this week, macro data points may not have the impact they usually do. Still, a host of inflation data points are on tap after last week’s generally decent employment updates.

Monday is quiet with Fed speak from Kugler (a dove) Monday morning with Treasury bill auctions thereafter.

February’s Consumer Credit Change hits in the afternoon, and we’ll get the final update on Manheim used vehicle prices.

The Manheim Index has been encouraging lately, pointing to stagnant auto prices, which, along with the crash in eggs, should help keep CPI in check.

Tuesday’s primary catalyst will be the March NFIB Small Business Optimism Index’s release.

It has been the holdout vibes gauge that remains above average, but small-business fervor cooled sharply in January and February after printing a multi-year high after President Trump’s November win.

It leans Republican, so this could be a decent barometer of how much pressure may be put on Trump to reverse his stern trade policy.

We’ll also get the weekly Johnson Redbook Retail Sales report—it fell notably last week, so our team will monitor it for confirmation on Tuesday morning.

The Fed’s Daly (a dove) speaks in the afternoon.

Wednesday’s key macro catalyst is the FOMC Minutes, which publishes at 2 p.m. ET.

Investors will be curious to read what the voting members discussed at the March Fed meeting and how much tariffs played into their dots.

Before the bell, Delta Airlines (DAL) kicks off the Q1 earnings season, with the big banks reporting Friday morning.

Wednesday is also when the new country-specific tariffs go into effect, but we think there will be tweaks in the timing and rates as the president negotiates.

Thursday is CPI Day.

The consensus calls for a 0.1% rise in the headline rate and a 0.3% jump in the core rate. That would bring the year-on-year totals to 2.6% and 3.0%, respectively.

Cool numbers would lift expectations for a May cut, and investors want to see that now, given the shaky macro foundation.

Jobless Claims and Fed speak come in the morning, too.

Friday’s focus will be on bank earnings in the pre-market, but PPI then takes the spotlight.

We could actually see some wholesale price deflation for March—something to keep an eye on.

The first full week of the second quarter wraps up with the April preliminary University of Michigan Surveys of Consumers, which is widely expected to show dreadful sentiment readings and high inflation outlooks.

In reality, the US 10-year breakeven inflation rate has cratered to 2.18% on the back of the oil price plunge—the lowest since last September.

Fiscal Policy Framework

Effective April 5, a universal 10% tariff applied to all imports, with higher reciprocal rates targeting specific counties starting April 9. With extremely high levies on Chinese goods and auto imports, the near-term aim is to raise revenue to fund later tax cuts. International tensions will be high, but nations will likely reach out to President Trump to reduce overall tariff rates.

Our team is also on watch for a global coordinated effort to appease Trump, which could introduce true free trade sooner than what so many pessimists expect. Countermeasures from China could be the first of several near-term retaliatory tariffs, but other nations just don’t hold the leverage—a protracted period of high tariffs poses depression-like risks to countries dependent upon exports.

It’s also possible that President Trump will offer tax credits and exemptions to US companies that have played by the rules by shifting production out of China in the past decade. We believe it’s important to call out that Trump said, “The markets are going to boom,” while aboard Air Force One late last week, so a Trump put may still exist.

Meanwhile, Senate Republicans push forward with a budget resolution to tap the reconciliation process for tax and spending legislation; the GOP must extend Trump’s 2017 tax cuts.

Last week, special elections in Florida went in the Republicans’ favor, and it’s too early to take them and the Wisconsin Supreme Court race as 2026 bellwethers. What will be important, though, is any potential GOP Trump defection with the midterms 19 months away. With no third term expected, it will be challenging for RINO Republicans to exert forceful political pressure on the POTUS.

Risks & Opportunities

S&P 500 earnings estimates are very likely to be further trimmed with odds of recession ticking above 60%; that’s a negative headline risk in the weeks ahead

Corporate executives may likewise voice a cautionary tone in the upcoming earnings season, potentially resulting in backlash from Trump

We expect extremely downbeat sentiment numbers this week, but that may present an opportunity to add on risk from a contrarian perspective

Weak inflation numbers on Thursday and Friday would increase rate-cut chances, and a Fed put could come sooner than later

A drop below 5000 on the S&P 500 could quickly lead to a test of the 4918 –20% psychological bear-market level

Quick Hits

The S&P 500 lost 10.5% between Thursday and Friday; 2-day declines of that magnitude were only seen in October 1987, November 2008, and March 2020 (since 1980)

The SPX is off to its 6th worst start to a year since 1950 (-13.7%); in comparable years, returns were strong for the balance of the year

The average US large-cap stock is down 20.3% YTD

The S&P 500 closed below its 38.2% Fibonacci retracement level of 5133, with the –20% bear market threshold at 4918, 3% below Friday’s settle

US and European large caps typically fall 30-35% during recessions

The VIX settled above 45 for the week—only seen before in October 2008-March 2009 and March 2020

The Nasdaq Composite is now below where it traded in November 2021, the Russell 2000 is within earshot of its August 2018 high, and international stocks are below prices from June 2021

The Cboe reported record put option trading volume on Thursday and Friday; record NYSE volume occurred Friday

Mortgage rates declined to a six-month low at 6.55%

Related Articles

AJ Giannone, CFA

Week of April 14, 2025

Retail sales in focus as volatility shakes markets. Tariff shifts, inflation data, and soaring tech stocks set the stage for another wild macro week

AJ Giannone, CFA

Week of April 7, 2025

CPI, PPI, FOMC minutes, tariff impact, and earnings in focus amid historic market selloff, soaring VIX, and rising recession odds—volatility intensifies.

Joseph Gradante, Allio CEO

Week of March 31, 2025

A high-stakes week in markets: jobs data, tariffs, and Powell’s speech take center stage. Key macro signals could shape Q2 momentum and recession odds.

AJ Giannone, CFA

Week of April 14, 2025

Retail sales in focus as volatility shakes markets. Tariff shifts, inflation data, and soaring tech stocks set the stage for another wild macro week

AJ Giannone, CFA

Week of April 7, 2025

CPI, PPI, FOMC minutes, tariff impact, and earnings in focus amid historic market selloff, soaring VIX, and rising recession odds—volatility intensifies.

Disclosures

This material is for informational purposes only and should not be construed as financial, legal, or tax advice. You should consult your own financial, legal, and tax advisors before engaging in any transaction. Information, including hypothetical projections of finances, may not take into account taxes, commissions, or other factors which may significantly affect potential outcomes. This material should not be considered an offer or recommendation to buy or sell a security. While information and sources are believed to be accurate, Allio Capital does not guarantee the accuracy or completeness of any information or source provided herein and is under no obligation to update this information.

Past performance is not a guarantee or a reliable indicator of future results. All investments contain risk and may lose value. Performance could be volatile; an investment in a fund or an account may lose money.

There is no guarantee that these investment strategies will work under all market conditions or are appropriate for all investors and each investor should evaluate their ability to invest long-term, especially during periods of downturn in the market.

This advertisement is provided by Allio Capital for informational purposes only and should not be considered investment advice, a recommendation, or a solicitation to buy or sell any securities. Investment decisions should be based on your specific financial situation and objectives, considering the risks and uncertainties associated with investing.

The views and forecasts expressed are those of Allio Capital and are subject to change without notice. Past performance is not indicative of future results, and investing involves risk, including the possible loss of principal. Market volatility, economic conditions, and changes in government policy may impact the accuracy of these forecasts and the performance of any investment.

Allio Capital utilizes proprietary technologies and methodologies, but no investment strategy can guarantee returns or eliminate risk. Investors should carefully consider their investment goals, risk tolerance, and financial circumstances before investing.

For more detailed information about our strategies and associated risks, please refer to the full disclosures available on our website or contact an Allio Capital advisor.

For informational purposes only; not personalized investment advice. All investments involve risk of loss. Past performance of any index or strategy is not indicative of future results. Any projections or forward-looking statements are hypothetical and not guaranteed. Allio is an SEC-registered investment adviser – see our Form ADV for details. No content should be construed as a recommendation to buy or sell any security.

Disclosures

This material is for informational purposes only and should not be construed as financial, legal, or tax advice. You should consult your own financial, legal, and tax advisors before engaging in any transaction. Information, including hypothetical projections of finances, may not take into account taxes, commissions, or other factors which may significantly affect potential outcomes. This material should not be considered an offer or recommendation to buy or sell a security. While information and sources are believed to be accurate, Allio Capital does not guarantee the accuracy or completeness of any information or source provided herein and is under no obligation to update this information.

Past performance is not a guarantee or a reliable indicator of future results. All investments contain risk and may lose value. Performance could be volatile; an investment in a fund or an account may lose money.

There is no guarantee that these investment strategies will work under all market conditions or are appropriate for all investors and each investor should evaluate their ability to invest long-term, especially during periods of downturn in the market.

This advertisement is provided by Allio Capital for informational purposes only and should not be considered investment advice, a recommendation, or a solicitation to buy or sell any securities. Investment decisions should be based on your specific financial situation and objectives, considering the risks and uncertainties associated with investing.

The views and forecasts expressed are those of Allio Capital and are subject to change without notice. Past performance is not indicative of future results, and investing involves risk, including the possible loss of principal. Market volatility, economic conditions, and changes in government policy may impact the accuracy of these forecasts and the performance of any investment.

Allio Capital utilizes proprietary technologies and methodologies, but no investment strategy can guarantee returns or eliminate risk. Investors should carefully consider their investment goals, risk tolerance, and financial circumstances before investing.

For more detailed information about our strategies and associated risks, please refer to the full disclosures available on our website or contact an Allio Capital advisor.

For informational purposes only; not personalized investment advice. All investments involve risk of loss. Past performance of any index or strategy is not indicative of future results. Any projections or forward-looking statements are hypothetical and not guaranteed. Allio is an SEC-registered investment adviser – see our Form ADV for details. No content should be construed as a recommendation to buy or sell any security.

Disclosures

This material is for informational purposes only and should not be construed as financial, legal, or tax advice. You should consult your own financial, legal, and tax advisors before engaging in any transaction. Information, including hypothetical projections of finances, may not take into account taxes, commissions, or other factors which may significantly affect potential outcomes. This material should not be considered an offer or recommendation to buy or sell a security. While information and sources are believed to be accurate, Allio Capital does not guarantee the accuracy or completeness of any information or source provided herein and is under no obligation to update this information.

Past performance is not a guarantee or a reliable indicator of future results. All investments contain risk and may lose value. Performance could be volatile; an investment in a fund or an account may lose money.

There is no guarantee that these investment strategies will work under all market conditions or are appropriate for all investors and each investor should evaluate their ability to invest long-term, especially during periods of downturn in the market.

This advertisement is provided by Allio Capital for informational purposes only and should not be considered investment advice, a recommendation, or a solicitation to buy or sell any securities. Investment decisions should be based on your specific financial situation and objectives, considering the risks and uncertainties associated with investing.

The views and forecasts expressed are those of Allio Capital and are subject to change without notice. Past performance is not indicative of future results, and investing involves risk, including the possible loss of principal. Market volatility, economic conditions, and changes in government policy may impact the accuracy of these forecasts and the performance of any investment.

Allio Capital utilizes proprietary technologies and methodologies, but no investment strategy can guarantee returns or eliminate risk. Investors should carefully consider their investment goals, risk tolerance, and financial circumstances before investing.

For more detailed information about our strategies and associated risks, please refer to the full disclosures available on our website or contact an Allio Capital advisor.

For informational purposes only; not personalized investment advice. All investments involve risk of loss. Past performance of any index or strategy is not indicative of future results. Any projections or forward-looking statements are hypothetical and not guaranteed. Allio is an SEC-registered investment adviser – see our Form ADV for details. No content should be construed as a recommendation to buy or sell any security.

What We Do

What We Say

Who We Are

Legal

Allio Advisors LLC ("Allio") is an SEC registered investment advisor. By using this website, you accept our Terms of Use and our Privacy Policy. Allio's investment advisory services are available only to residents of the United States. Nothing on this website should be considered an offer, recommendation, solicitation of an offer, or advice to buy or sell any security. The information provided herein is for informational and general educational purposes only and is not investment or financial advice. Additionally, Allio does not provide tax advice and investors are encouraged to consult with their tax advisor. By law, we must provide investment advice that is in the best interest of our client. Please refer to Allio's ADV Part 2A Brochure for important additional information. Please see our Customer Relationship Summary.

Online trading has inherent risk due to system response, execution price, speed, liquidity, market data and access times that may vary due to market conditions, system performance, market volatility, size and type of order and other factors. An investor should understand these and additional risks before trading. Any historical returns, expected returns, or probability projections are hypothetical in nature and may not reflect actual future performance. Past performance is no guarantee of future results.

Brokerage services will be provided to Allio clients through Allio Markets LLC, ("Allio Markets") SEC-registered broker-dealer and member FINRA/SIPC . Securities in your account protected up to $500,000. For details, please see www.sipc.org. Allio Advisors LLC and Allio Markets LLC are separate but affiliated companies.

Securities products are: Not FDIC insured · Not bank guaranteed · May lose value

Any investment , trade-related or brokerage questions shall be communicated to support@alliocapital.com

Please read Important Legal Disclosures

v1 01.20.2025

What We Do

What We Say

Who We Are

Legal

Allio Advisors LLC ("Allio") is an SEC registered investment advisor. By using this website, you accept our Terms of Use and our Privacy Policy. Allio's investment advisory services are available only to residents of the United States. Nothing on this website should be considered an offer, recommendation, solicitation of an offer, or advice to buy or sell any security. The information provided herein is for informational and general educational purposes only and is not investment or financial advice. Additionally, Allio does not provide tax advice and investors are encouraged to consult with their tax advisor. By law, we must provide investment advice that is in the best interest of our client. Please refer to Allio's ADV Part 2A Brochure for important additional information. Please see our Customer Relationship Summary.

Online trading has inherent risk due to system response, execution price, speed, liquidity, market data and access times that may vary due to market conditions, system performance, market volatility, size and type of order and other factors. An investor should understand these and additional risks before trading. Any historical returns, expected returns, or probability projections are hypothetical in nature and may not reflect actual future performance. Past performance is no guarantee of future results.

Brokerage services will be provided to Allio clients through Allio Markets LLC, ("Allio Markets") SEC-registered broker-dealer and member FINRA/SIPC . Securities in your account protected up to $500,000. For details, please see www.sipc.org. Allio Advisors LLC and Allio Markets LLC are separate but affiliated companies.

Securities products are: Not FDIC insured · Not bank guaranteed · May lose value

Any investment , trade-related or brokerage questions shall be communicated to support@alliocapital.com

Please read Important Legal Disclosures

v1 01.20.2025

What We Do

What We Say

Who We Are

Legal

Allio Advisors LLC ("Allio") is an SEC registered investment advisor. By using this website, you accept our Terms of Use and our Privacy Policy. Allio's investment advisory services are available only to residents of the United States. Nothing on this website should be considered an offer, recommendation, solicitation of an offer, or advice to buy or sell any security. The information provided herein is for informational and general educational purposes only and is not investment or financial advice. Additionally, Allio does not provide tax advice and investors are encouraged to consult with their tax advisor. By law, we must provide investment advice that is in the best interest of our client. Please refer to Allio's ADV Part 2A Brochure for important additional information. Please see our Customer Relationship Summary.

Online trading has inherent risk due to system response, execution price, speed, liquidity, market data and access times that may vary due to market conditions, system performance, market volatility, size and type of order and other factors. An investor should understand these and additional risks before trading. Any historical returns, expected returns, or probability projections are hypothetical in nature and may not reflect actual future performance. Past performance is no guarantee of future results.

Brokerage services will be provided to Allio clients through Allio Markets LLC, ("Allio Markets") SEC-registered broker-dealer and member FINRA/SIPC . Securities in your account protected up to $500,000. For details, please see www.sipc.org. Allio Advisors LLC and Allio Markets LLC are separate but affiliated companies.

Securities products are: Not FDIC insured · Not bank guaranteed · May lose value

Any investment , trade-related or brokerage questions shall be communicated to support@alliocapital.com

Please read Important Legal Disclosures

v1 01.20.2025