The

MacroEconomic Calendar

The MacroEconomic Calendar

Apr 21, 2025

Week of April 21, 2025

Week of April 21, 2025

AJ Giannone, CFA

The Setup & Where to Focus

The S&P 500 gave back modest ground during the holiday-shortened week.

US large caps lost 1.5%, dragged down once again by big tech. The Nasdaq Composite fell 2.6% after initially outperforming off the early-April lows.

The Mag 7 ETF (MAGS), specifically, shed 5.3% and is only a few percentage points from its weekly closing low, still in bear-market territory, down 27% from the December 2024 all-time high.

Ahead of Netflix’s (NFLX) impressive Q1 report last Thursday night, all the Mag 7 components closed lower last week—NVIDIA (NVDA) was the worst of the bunch, down 8.5%, thanks in large part to a 7% Wednesday drop associated with President Trump’s chip export restriction news.

Despite the S&P 500’s retreat, the Cboe Volatility Index (VIX) tumbled three points, now below 30 for the first time on a weekly closing basis since last month.

It appears large traders have layered on significant protection post Liberation Day. A 30 VIX implies about a 2% daily SPX swing.

Earnings season kicks into high gear this week with Q1 reports from Tesla (TSLA) and Alphabet (GOOGL).

Digging into the sectors, it was the smaller spots that soared.

Real Estate (XLRE) rallied 4% over the four-day period, nearly clocking in its best week since December 2023. Typically, rising and volatile interest rates are a headwind for the property niche, but Real Estate has turned somewhat defensive this month.

Of course, a nearly 16-basis-point drop in the benchmark 10-year Treasury note yield was a tailwind for REITs. Year to date, XLRE has offered significant diversification benefits—up by 0.1%, dividends included, versus the S&P 500 ETF’s (SPY) -9.9% total return. Real Estate is just 2.3% of the SPX.

Energy (XLE)—only 3.4% of the US large cap index—rallied 3.2%. WTI crude oil gained 5.2%, its second-best week of 2025. US oil notched a low of $56.06 during the throes of the tariff-induced panic selling, and that may turn out to be a durable bottom based on the look of the chart.

A weaker dollar surely helped, but so too did geopolitical tensions in the Middle East—tighter US sanctions against Iranian crude supported oil. Still, the supply/demand balance doesn’t look overly bullish—Fitch Ratings lowered its forecasts for WTI and Brent on lower economic growth for the balance of the year and production increases from OPEC+ members.

Dragging the S&P 500 lower ahead of Good Friday and the Easter weekend was mega-cap tech.

Information Technology (XLK) fell 3.7%, Consumer Discretionary (XLY), and Communication Services (XLC)—the three growth sectors—offset what was otherwise a strong week for global stocks.

Valuations for the Mag 7 continue coming in, and these multinational corporations are at the center of the tariff storm. Other problems have emerged, too. GOOGL dropped in each session from Tuesday through Thursday, highlighted by a dip after a US district judge ruled that the company was responsible for intentionally building and sustaining a monopoly in the digital ad-network market.

The hits just keep on coming for the mega caps, which collectively trade with a P/E multiple of 22—the lowest in more than two years. The focus now shifts to Q1 earnings which will have a major impact on the S&P 500 writ large.

As large caps wobbled, small caps staged a rally.

The iShares Russell 2000 ETF (IWM) rose 1.2%, backing up a high-volume advance from the previous week. Calmer times in the bond market were a boon, but both domestic small and mid-cap equities sport P/E ratios near recession/bear market levels (between 13x-14x).

Regional banks—a large segment of the small-cap index—posted generally solid results in the face of a highly uncertain macro backdrop. The SPDR S&P Regional Banking ETF (KRE) rose 4.4% for the week, making it back-to-back weekly rallies. Biotech (XBI) was up, too.

Turning to international markets, the Vanguard FTSE All-World ex-US ETF (VEU) gained 2.1% and is now 11.5% above its April low; foreign stocks are actually closer to their 52-week high than the 52-week bottom.

Once again, the sagging greenback helps, but broad weakness in mega-cap tech acts as an alpha-generator for VEU versus the SPX. Moreover, many country funds across Europe and Latin America boast downright bullish years. Spain (EWP), Germany (EWG), Mexico (EWW), Italy (EWI), and Brazil (EWZ) are all up 12% or more in 2025.

Geographical diversification felt left for dead at the end of last year, but portfolios with global exposure have, for now, contributed to recent relative strength.

We believe current trends could continue through 2025, though economic conditions may evolve. The U.S. may be positioned for improvement depending on various macro developments.

Not to bury the lead any further, but all eyes remain on the US bond market.

The 10-year rate is now 4.33%, down 26 basis points from this month’s peak.

Now, the financial media would have you believe that interest rates have soared to levels not seen in years thanks to President Trump’s aggressive trade policies. The evidence tells a different story.

Zoom out the 10-year's chart a few years, and we find that the benchmark Treasury rate has ranged from about 3.25% to 5.00%. Today’s yield is close to the middle of that zone despite the drama.

Furthermore, the yield curve is close to normal (aside from a slight inversion on the front end). Ignore the noise, and a 3.8% 2-year, 4.3% 10-year, and 4.8% 30-year is a relatively typical term structure.

There are risks, such as a rising term premium for long-dated Treasuries and a high bond market volatility index (MOVE). The high yield spread rose after Liberation Day, but some of the increase has been pared in the last few sessions.

Commodities have broadly acted as a risk-on/risk-off indicator this year; oil’s April drop and pop indicates the correlation with stocks.

We think it’s possible that commodities could catch a more enduring bid if the US Dollar Index (DXY) declines further.

The DXY settled at 99.23 last Friday—its worst weekly finish in over three years. Long-term support is between 89 and 90. Like with interest rates, while the dollar’s move has felt intense, the index is merely in the middle of an 11-year trading range.

What’s not normal is what is going on with gold. The precious metal has been up in all but two weeks of 2025. Its $3326 close last week was easily an all-time high, and gold is now above its 1980 inflation-adjusted peak.

Off to its best start to a year since 1974, ‘long gold’ was ranked as the most over-crowded trade in Bank of America Global Research’s April Fund Manager Survey. Through Good Friday, gold had returned 27% in 2025—more than 36 percentage points of alpha compared to the SPX.

Central banks continue buying gold en masse—China is potentially a huge buyer as it sells Treasuries and dollars.

Finally, despite a few days of volatility during the stock market turmoil two weeks ago, bitcoin has wrapped around the $85,000 level—a rally through $90,000 could spark a significant rally.

Weekly Calendar Look Ahead

It’s a light data week on Wall Street—between Retail Sales last week and the PCE report to close out the month and a ton of jobs data on May 1 and 2.

Once again, traders’ focus will be on headlines from the White House, but key earnings reports and conference calls are sure to offer clues on the macro.

We’ve already seen some companies offer unusual bi-modal EPS outlooks—one assuming modest tariffs and another factoring in very high global levies.

With bank earnings in hand, the numbers and vibes thus far are better than feared. But let’s get to the economic data.

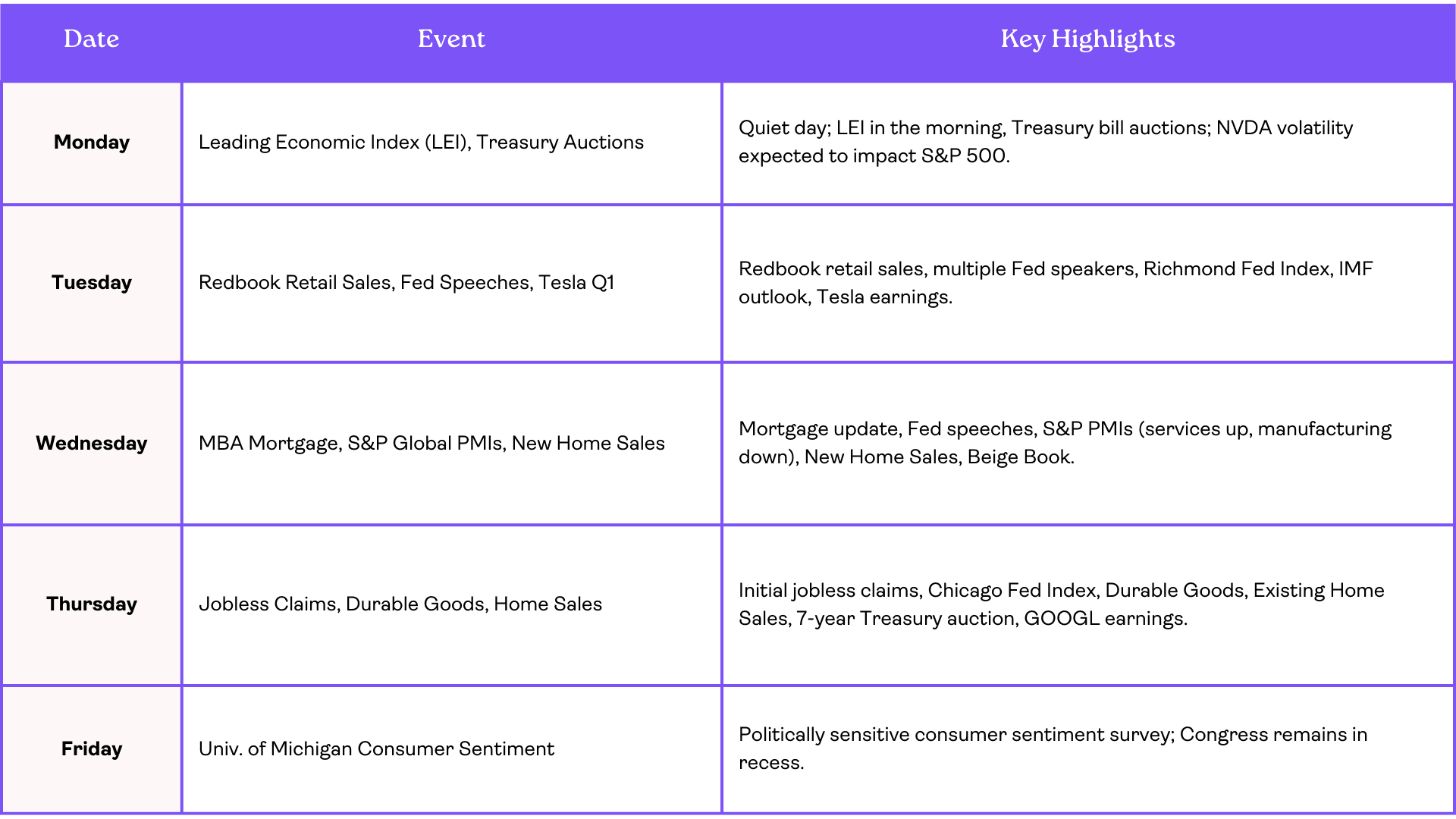

Monday is quiet, with just the Leading Economic Index (LEI) published by The Conference Board in the morning, followed by Treasury bill auctions. NVDA’s implied volatility ratcheted up last week, so it will likely play an outsized role in the S&P 500’s day-to-day movements.

Tuesday is another somewhat uneventful data slate, but the weekly Johnson Redbook retail sales update is particularly interesting at the moment, given consumers’ apparent stockpiling ahead of tariffs.

The previous two Redbooks were strong, and last week’s March Retail Sales report published by the Census Bureau was firm. On the one hand, the economy before Liberation Day appeared to be on a decent footing with resilient hard data, but the bears suggest that April will be a far different story.

One arbiter could be the prediction markets—bettors price in a healthy 168,000 payrolls gain for the current month. We will know for sure on Friday, May 2.

Fed speak is also heavy on Tuesday, with Jefferson, Harker, Kashkari, and Kugler all hitting the circuit. We’ll dig into it later, but Chair Powell was almost combative with his words last week in response to aggressive jawboning from President Trump.

The chance of a May rate cut has dwindled amid uncertainty as to the extent to which tariffs will impact consumer prices.

Tuesday morning’s slate includes the April Richmond Fed Manufacturing Index—soft survey data—and the March Money Supply figure in the afternoon.

The IMF releases its full World Economic Outlook and Global Financial Stability update, likely in the morning. Tesla reports earnings after the bell.

Wednesday is a bit busier.

The weekly MBA mortgage market update comes out early, followed by Fed speaking engagements from Beth, Goolsbee, and Waller.

After the bell, we get S&P Global Flash PMIs for April, which are expected to show expansion in Services but a modest contraction in Manufacturing. New Home Sales comes at 10 a.m. ET, and a slight month-over-month increase is seen.

We expect volatility throughout the morning, given the trio of Fed speeches and among the first key macro reports for April—after the Liberation Day announcement from the White House Rose Garden.

In the afternoon, the Fed’s Beige Book of regional economic conditions prints could also act as an early soft-data gauge of the trade war’s impact.

Thursday offers clues on the labor and housing markets.

Initial Jobless Claims were light once again last week, suggesting that despite uncertainty in the C-suite, there is no evidence of mass layoffs. So long as people are employed and earning positive real wages, they are likely to continue spending.

Along with the Chicago Fed National Activity Index, March Durable Goods numbers cross the wires in the premarket.

Existing Home Sales hits after the bell, and a sequential decline is anticipated.

Our team will monitor the 7-year Treasury auction at 1 p.m. ET for potential volatility in the bond market.

Kashkari speaks again in the evening, right after GOOGL results.

Friday’s highlight is the politically tainted University of Michigan Surveys of Consumers report, April’s preliminary.

Fiscal Policy Framework

Congress continues its recess, but that doesn’t mean there isn’t drama between Capitol Hill, The Federal Reserve, and the White House. Trump controlled the media narrative last week, Truth Social-ing his displeasure with Powell. The POTUS is reportedly considering methods to remove the Fed Chair, but he cannot terminate him without cause; simply disagreeing with interest rate policy is insufficient grounds for dismissal. Of course, the Fed officials’ failure to hit the 2% inflation target, out-of-control money printing, and aggressively cutting rates in late 2024 while putting off balance sheet reduction until after the election were notable failures.

It’s totally normal for a president to verbally bully the FOMC, but threatening their job is something different. Alas, Powell’s term ends in 13 months, so we see Trump’s stance as an effort to influence policy, not dictate it. The president outlined what the European Central Bank should do, applauding the ECB for cutting rates, asserting that the US FOMC should follow their lead.

The White House may be teeing up Powell to be a scapegoat of sorts if the economy turns south. Keep in mind that Powell and Treasury Secretary Bessent meet up for breakfast once per week (as is tradition), so drama backstage is likely much less compared to public missives—Trump's Truth Social and Powell referencing “Ferris Bueller’s Day Off” (and Smoot-Hawley) last week.

On the trade front, we have been expecting a more unified bloc against China to be the next stage of the trade war, which appears to be unfolding. The US urges allies to isolate Beijing and restrict Chinese exports. Given current levies, the US and China have a near-embargo in certain areas of trade. There are even whispers that Bessent could work to delist Chinese stocks from domestic exchanges—that would be a major macro event, but we see it is a low probability. We still don’t know how sectoral tariffs—those on semiconductors, pharmaceuticals, and minerals—will shake out.

Upon Congress getting back to work, the focus will be the budget. Speaker Mike Johnson has a self-imposed Memorial Day deadline for completing a big, beautiful bill. The debt ceiling debate will probably rear its head again this summer as conservatives in the House demand major spending cuts. All the while, Trump’s approval is a net –4, far better than the average of his first term and way ahead of Congress’ net approval.

Risks and Opportunities

The S&P 500 now trades 19x forward EPS estimates, between the 5-year and 10-year averages. CY 2025 per-share earnings forecasts keep retreating, though, and the sum could end up being closer to $260 if historical analogs play out. Even if we get a 10% EPS recovery in 2026, that would leave the SPX 18.5x forward estimates by the close of this year, which is likely close to a fair P/E.

Technically, 5500 is a key spot on the chart for the S&P 500. It’s the 50% retracement of the February-April decline, the mid-March low, and where the index paused after the 10% up day back on the 9th of the month.

So, there are valuation and technical risks with US large caps. There may be opportunities elsewhere. We previously noted cheap valuations in domestic SMID caps, and foreign stocks (also inexpensive) have firm relative strength.

A weaker dollar would support international equities, but Allio is watching the DXY as it straddles key support between 99-101.

Recent market developments aligned with previous observations, although continued volatility remains a possibility. Corrections and bear markets are known to see periods of relative tranquility—the next two and a half weeks will be key given the bevy of major earnings updates, the April jobs report, and the May 7 FOMC meeting. Should markets remain stable through upcoming events, there could be potential for further gains, though risks remain.

Gold’s bid appears strong, with intraday selling bouts being temporary. Assuming China is a price-insensitive buyer, pullbacks may offer potential entry points, depending on investor risk tolerance and long-term strategy.

Quick Hits

The S&P 500 is down 10% through 2025’s first 73 trading days, the 5th worst start to a year on record

The dollar is off to its second-weakest beginning to a year in the last three decades

While economic uncertainty is high, forward equity returns have been strong in similar instances

Four Fed rate cuts are priced into the next 12 months

Citi’s Earnings Revision Index is the lowest in five years

BofA reports EPFR data show the biggest foreign selling of US corporate bonds since April 2020, while inflows to gold notched a record

US gas prices are 45 cents below year-ago levels as the travel season gets going

The Setup & Where to Focus

The S&P 500 gave back modest ground during the holiday-shortened week.

US large caps lost 1.5%, dragged down once again by big tech. The Nasdaq Composite fell 2.6% after initially outperforming off the early-April lows.

The Mag 7 ETF (MAGS), specifically, shed 5.3% and is only a few percentage points from its weekly closing low, still in bear-market territory, down 27% from the December 2024 all-time high.

Ahead of Netflix’s (NFLX) impressive Q1 report last Thursday night, all the Mag 7 components closed lower last week—NVIDIA (NVDA) was the worst of the bunch, down 8.5%, thanks in large part to a 7% Wednesday drop associated with President Trump’s chip export restriction news.

Despite the S&P 500’s retreat, the Cboe Volatility Index (VIX) tumbled three points, now below 30 for the first time on a weekly closing basis since last month.

It appears large traders have layered on significant protection post Liberation Day. A 30 VIX implies about a 2% daily SPX swing.

Earnings season kicks into high gear this week with Q1 reports from Tesla (TSLA) and Alphabet (GOOGL).

Digging into the sectors, it was the smaller spots that soared.

Real Estate (XLRE) rallied 4% over the four-day period, nearly clocking in its best week since December 2023. Typically, rising and volatile interest rates are a headwind for the property niche, but Real Estate has turned somewhat defensive this month.

Of course, a nearly 16-basis-point drop in the benchmark 10-year Treasury note yield was a tailwind for REITs. Year to date, XLRE has offered significant diversification benefits—up by 0.1%, dividends included, versus the S&P 500 ETF’s (SPY) -9.9% total return. Real Estate is just 2.3% of the SPX.

Energy (XLE)—only 3.4% of the US large cap index—rallied 3.2%. WTI crude oil gained 5.2%, its second-best week of 2025. US oil notched a low of $56.06 during the throes of the tariff-induced panic selling, and that may turn out to be a durable bottom based on the look of the chart.

A weaker dollar surely helped, but so too did geopolitical tensions in the Middle East—tighter US sanctions against Iranian crude supported oil. Still, the supply/demand balance doesn’t look overly bullish—Fitch Ratings lowered its forecasts for WTI and Brent on lower economic growth for the balance of the year and production increases from OPEC+ members.

Dragging the S&P 500 lower ahead of Good Friday and the Easter weekend was mega-cap tech.

Information Technology (XLK) fell 3.7%, Consumer Discretionary (XLY), and Communication Services (XLC)—the three growth sectors—offset what was otherwise a strong week for global stocks.

Valuations for the Mag 7 continue coming in, and these multinational corporations are at the center of the tariff storm. Other problems have emerged, too. GOOGL dropped in each session from Tuesday through Thursday, highlighted by a dip after a US district judge ruled that the company was responsible for intentionally building and sustaining a monopoly in the digital ad-network market.

The hits just keep on coming for the mega caps, which collectively trade with a P/E multiple of 22—the lowest in more than two years. The focus now shifts to Q1 earnings which will have a major impact on the S&P 500 writ large.

As large caps wobbled, small caps staged a rally.

The iShares Russell 2000 ETF (IWM) rose 1.2%, backing up a high-volume advance from the previous week. Calmer times in the bond market were a boon, but both domestic small and mid-cap equities sport P/E ratios near recession/bear market levels (between 13x-14x).

Regional banks—a large segment of the small-cap index—posted generally solid results in the face of a highly uncertain macro backdrop. The SPDR S&P Regional Banking ETF (KRE) rose 4.4% for the week, making it back-to-back weekly rallies. Biotech (XBI) was up, too.

Turning to international markets, the Vanguard FTSE All-World ex-US ETF (VEU) gained 2.1% and is now 11.5% above its April low; foreign stocks are actually closer to their 52-week high than the 52-week bottom.

Once again, the sagging greenback helps, but broad weakness in mega-cap tech acts as an alpha-generator for VEU versus the SPX. Moreover, many country funds across Europe and Latin America boast downright bullish years. Spain (EWP), Germany (EWG), Mexico (EWW), Italy (EWI), and Brazil (EWZ) are all up 12% or more in 2025.

Geographical diversification felt left for dead at the end of last year, but portfolios with global exposure have, for now, contributed to recent relative strength.

We believe current trends could continue through 2025, though economic conditions may evolve. The U.S. may be positioned for improvement depending on various macro developments.

Not to bury the lead any further, but all eyes remain on the US bond market.

The 10-year rate is now 4.33%, down 26 basis points from this month’s peak.

Now, the financial media would have you believe that interest rates have soared to levels not seen in years thanks to President Trump’s aggressive trade policies. The evidence tells a different story.

Zoom out the 10-year's chart a few years, and we find that the benchmark Treasury rate has ranged from about 3.25% to 5.00%. Today’s yield is close to the middle of that zone despite the drama.

Furthermore, the yield curve is close to normal (aside from a slight inversion on the front end). Ignore the noise, and a 3.8% 2-year, 4.3% 10-year, and 4.8% 30-year is a relatively typical term structure.

There are risks, such as a rising term premium for long-dated Treasuries and a high bond market volatility index (MOVE). The high yield spread rose after Liberation Day, but some of the increase has been pared in the last few sessions.

Commodities have broadly acted as a risk-on/risk-off indicator this year; oil’s April drop and pop indicates the correlation with stocks.

We think it’s possible that commodities could catch a more enduring bid if the US Dollar Index (DXY) declines further.

The DXY settled at 99.23 last Friday—its worst weekly finish in over three years. Long-term support is between 89 and 90. Like with interest rates, while the dollar’s move has felt intense, the index is merely in the middle of an 11-year trading range.

What’s not normal is what is going on with gold. The precious metal has been up in all but two weeks of 2025. Its $3326 close last week was easily an all-time high, and gold is now above its 1980 inflation-adjusted peak.

Off to its best start to a year since 1974, ‘long gold’ was ranked as the most over-crowded trade in Bank of America Global Research’s April Fund Manager Survey. Through Good Friday, gold had returned 27% in 2025—more than 36 percentage points of alpha compared to the SPX.

Central banks continue buying gold en masse—China is potentially a huge buyer as it sells Treasuries and dollars.

Finally, despite a few days of volatility during the stock market turmoil two weeks ago, bitcoin has wrapped around the $85,000 level—a rally through $90,000 could spark a significant rally.

Weekly Calendar Look Ahead

It’s a light data week on Wall Street—between Retail Sales last week and the PCE report to close out the month and a ton of jobs data on May 1 and 2.

Once again, traders’ focus will be on headlines from the White House, but key earnings reports and conference calls are sure to offer clues on the macro.

We’ve already seen some companies offer unusual bi-modal EPS outlooks—one assuming modest tariffs and another factoring in very high global levies.

With bank earnings in hand, the numbers and vibes thus far are better than feared. But let’s get to the economic data.

Monday is quiet, with just the Leading Economic Index (LEI) published by The Conference Board in the morning, followed by Treasury bill auctions. NVDA’s implied volatility ratcheted up last week, so it will likely play an outsized role in the S&P 500’s day-to-day movements.

Tuesday is another somewhat uneventful data slate, but the weekly Johnson Redbook retail sales update is particularly interesting at the moment, given consumers’ apparent stockpiling ahead of tariffs.

The previous two Redbooks were strong, and last week’s March Retail Sales report published by the Census Bureau was firm. On the one hand, the economy before Liberation Day appeared to be on a decent footing with resilient hard data, but the bears suggest that April will be a far different story.

One arbiter could be the prediction markets—bettors price in a healthy 168,000 payrolls gain for the current month. We will know for sure on Friday, May 2.

Fed speak is also heavy on Tuesday, with Jefferson, Harker, Kashkari, and Kugler all hitting the circuit. We’ll dig into it later, but Chair Powell was almost combative with his words last week in response to aggressive jawboning from President Trump.

The chance of a May rate cut has dwindled amid uncertainty as to the extent to which tariffs will impact consumer prices.

Tuesday morning’s slate includes the April Richmond Fed Manufacturing Index—soft survey data—and the March Money Supply figure in the afternoon.

The IMF releases its full World Economic Outlook and Global Financial Stability update, likely in the morning. Tesla reports earnings after the bell.

Wednesday is a bit busier.

The weekly MBA mortgage market update comes out early, followed by Fed speaking engagements from Beth, Goolsbee, and Waller.

After the bell, we get S&P Global Flash PMIs for April, which are expected to show expansion in Services but a modest contraction in Manufacturing. New Home Sales comes at 10 a.m. ET, and a slight month-over-month increase is seen.

We expect volatility throughout the morning, given the trio of Fed speeches and among the first key macro reports for April—after the Liberation Day announcement from the White House Rose Garden.

In the afternoon, the Fed’s Beige Book of regional economic conditions prints could also act as an early soft-data gauge of the trade war’s impact.

Thursday offers clues on the labor and housing markets.

Initial Jobless Claims were light once again last week, suggesting that despite uncertainty in the C-suite, there is no evidence of mass layoffs. So long as people are employed and earning positive real wages, they are likely to continue spending.

Along with the Chicago Fed National Activity Index, March Durable Goods numbers cross the wires in the premarket.

Existing Home Sales hits after the bell, and a sequential decline is anticipated.

Our team will monitor the 7-year Treasury auction at 1 p.m. ET for potential volatility in the bond market.

Kashkari speaks again in the evening, right after GOOGL results.

Friday’s highlight is the politically tainted University of Michigan Surveys of Consumers report, April’s preliminary.

Fiscal Policy Framework

Congress continues its recess, but that doesn’t mean there isn’t drama between Capitol Hill, The Federal Reserve, and the White House. Trump controlled the media narrative last week, Truth Social-ing his displeasure with Powell. The POTUS is reportedly considering methods to remove the Fed Chair, but he cannot terminate him without cause; simply disagreeing with interest rate policy is insufficient grounds for dismissal. Of course, the Fed officials’ failure to hit the 2% inflation target, out-of-control money printing, and aggressively cutting rates in late 2024 while putting off balance sheet reduction until after the election were notable failures.

It’s totally normal for a president to verbally bully the FOMC, but threatening their job is something different. Alas, Powell’s term ends in 13 months, so we see Trump’s stance as an effort to influence policy, not dictate it. The president outlined what the European Central Bank should do, applauding the ECB for cutting rates, asserting that the US FOMC should follow their lead.

The White House may be teeing up Powell to be a scapegoat of sorts if the economy turns south. Keep in mind that Powell and Treasury Secretary Bessent meet up for breakfast once per week (as is tradition), so drama backstage is likely much less compared to public missives—Trump's Truth Social and Powell referencing “Ferris Bueller’s Day Off” (and Smoot-Hawley) last week.

On the trade front, we have been expecting a more unified bloc against China to be the next stage of the trade war, which appears to be unfolding. The US urges allies to isolate Beijing and restrict Chinese exports. Given current levies, the US and China have a near-embargo in certain areas of trade. There are even whispers that Bessent could work to delist Chinese stocks from domestic exchanges—that would be a major macro event, but we see it is a low probability. We still don’t know how sectoral tariffs—those on semiconductors, pharmaceuticals, and minerals—will shake out.

Upon Congress getting back to work, the focus will be the budget. Speaker Mike Johnson has a self-imposed Memorial Day deadline for completing a big, beautiful bill. The debt ceiling debate will probably rear its head again this summer as conservatives in the House demand major spending cuts. All the while, Trump’s approval is a net –4, far better than the average of his first term and way ahead of Congress’ net approval.

Risks and Opportunities

The S&P 500 now trades 19x forward EPS estimates, between the 5-year and 10-year averages. CY 2025 per-share earnings forecasts keep retreating, though, and the sum could end up being closer to $260 if historical analogs play out. Even if we get a 10% EPS recovery in 2026, that would leave the SPX 18.5x forward estimates by the close of this year, which is likely close to a fair P/E.

Technically, 5500 is a key spot on the chart for the S&P 500. It’s the 50% retracement of the February-April decline, the mid-March low, and where the index paused after the 10% up day back on the 9th of the month.

So, there are valuation and technical risks with US large caps. There may be opportunities elsewhere. We previously noted cheap valuations in domestic SMID caps, and foreign stocks (also inexpensive) have firm relative strength.

A weaker dollar would support international equities, but Allio is watching the DXY as it straddles key support between 99-101.

Recent market developments aligned with previous observations, although continued volatility remains a possibility. Corrections and bear markets are known to see periods of relative tranquility—the next two and a half weeks will be key given the bevy of major earnings updates, the April jobs report, and the May 7 FOMC meeting. Should markets remain stable through upcoming events, there could be potential for further gains, though risks remain.

Gold’s bid appears strong, with intraday selling bouts being temporary. Assuming China is a price-insensitive buyer, pullbacks may offer potential entry points, depending on investor risk tolerance and long-term strategy.

Quick Hits

The S&P 500 is down 10% through 2025’s first 73 trading days, the 5th worst start to a year on record

The dollar is off to its second-weakest beginning to a year in the last three decades

While economic uncertainty is high, forward equity returns have been strong in similar instances

Four Fed rate cuts are priced into the next 12 months

Citi’s Earnings Revision Index is the lowest in five years

BofA reports EPFR data show the biggest foreign selling of US corporate bonds since April 2020, while inflows to gold notched a record

US gas prices are 45 cents below year-ago levels as the travel season gets going

Related Articles

AJ Giannone, CFA

Week of April 21, 2025

S&P 500 slipped 1.5% as tech faltered, while real estate and energy outperformed. Gold hit record highs. Focus shifts to key earnings and Fed signals amid trade tensions. This 157-character summary captures the key market movements, sector performance, and upcoming focus areas from the article.

AJ Giannone, CFA

Week of April 14, 2025

Retail sales in focus as volatility shakes markets. Tariff shifts, inflation data, and soaring tech stocks set the stage for another wild macro week

AJ Giannone, CFA

Week of April 7, 2025

CPI, PPI, FOMC minutes, tariff impact, and earnings in focus amid historic market selloff, soaring VIX, and rising recession odds—volatility intensifies.

AJ Giannone, CFA

Week of April 21, 2025

S&P 500 slipped 1.5% as tech faltered, while real estate and energy outperformed. Gold hit record highs. Focus shifts to key earnings and Fed signals amid trade tensions. This 157-character summary captures the key market movements, sector performance, and upcoming focus areas from the article.

AJ Giannone, CFA

Week of April 14, 2025

Retail sales in focus as volatility shakes markets. Tariff shifts, inflation data, and soaring tech stocks set the stage for another wild macro week

Disclosures

This material is for informational purposes only and should not be construed as financial, legal, or tax advice. You should consult your own financial, legal, and tax advisors before engaging in any transaction. Information, including hypothetical projections of finances, may not take into account taxes, commissions, or other factors which may significantly affect potential outcomes. This material should not be considered an offer or recommendation to buy or sell a security. While information and sources are believed to be accurate, Allio Capital does not guarantee the accuracy or completeness of any information or source provided herein and is under no obligation to update this information.

Past performance is not a guarantee or a reliable indicator of future results. All investments contain risk and may lose value. Performance could be volatile; an investment in a fund or an account may lose money.

There is no guarantee that these investment strategies will work under all market conditions or are appropriate for all investors and each investor should evaluate their ability to invest long-term, especially during periods of downturn in the market.

This advertisement is provided by Allio Capital for informational purposes only and should not be considered investment advice, a recommendation, or a solicitation to buy or sell any securities. Investment decisions should be based on your specific financial situation and objectives, considering the risks and uncertainties associated with investing.

The views and forecasts expressed are those of Allio Capital and are subject to change without notice. Past performance is not indicative of future results, and investing involves risk, including the possible loss of principal. Market volatility, economic conditions, and changes in government policy may impact the accuracy of these forecasts and the performance of any investment.

Allio Capital utilizes proprietary technologies and methodologies, but no investment strategy can guarantee returns or eliminate risk. Investors should carefully consider their investment goals, risk tolerance, and financial circumstances before investing.

For more detailed information about our strategies and associated risks, please refer to the full disclosures available on our website or contact an Allio Capital advisor.

For informational purposes only; not personalized investment advice. All investments involve risk of loss. Past performance of any index or strategy is not indicative of future results. Any projections or forward-looking statements are hypothetical and not guaranteed. Allio is an SEC-registered investment adviser – see our Form ADV for details. No content should be construed as a recommendation to buy or sell any security.

Disclosures

This material is for informational purposes only and should not be construed as financial, legal, or tax advice. You should consult your own financial, legal, and tax advisors before engaging in any transaction. Information, including hypothetical projections of finances, may not take into account taxes, commissions, or other factors which may significantly affect potential outcomes. This material should not be considered an offer or recommendation to buy or sell a security. While information and sources are believed to be accurate, Allio Capital does not guarantee the accuracy or completeness of any information or source provided herein and is under no obligation to update this information.

Past performance is not a guarantee or a reliable indicator of future results. All investments contain risk and may lose value. Performance could be volatile; an investment in a fund or an account may lose money.

There is no guarantee that these investment strategies will work under all market conditions or are appropriate for all investors and each investor should evaluate their ability to invest long-term, especially during periods of downturn in the market.

This advertisement is provided by Allio Capital for informational purposes only and should not be considered investment advice, a recommendation, or a solicitation to buy or sell any securities. Investment decisions should be based on your specific financial situation and objectives, considering the risks and uncertainties associated with investing.

The views and forecasts expressed are those of Allio Capital and are subject to change without notice. Past performance is not indicative of future results, and investing involves risk, including the possible loss of principal. Market volatility, economic conditions, and changes in government policy may impact the accuracy of these forecasts and the performance of any investment.

Allio Capital utilizes proprietary technologies and methodologies, but no investment strategy can guarantee returns or eliminate risk. Investors should carefully consider their investment goals, risk tolerance, and financial circumstances before investing.

For more detailed information about our strategies and associated risks, please refer to the full disclosures available on our website or contact an Allio Capital advisor.

For informational purposes only; not personalized investment advice. All investments involve risk of loss. Past performance of any index or strategy is not indicative of future results. Any projections or forward-looking statements are hypothetical and not guaranteed. Allio is an SEC-registered investment adviser – see our Form ADV for details. No content should be construed as a recommendation to buy or sell any security.

Disclosures

This material is for informational purposes only and should not be construed as financial, legal, or tax advice. You should consult your own financial, legal, and tax advisors before engaging in any transaction. Information, including hypothetical projections of finances, may not take into account taxes, commissions, or other factors which may significantly affect potential outcomes. This material should not be considered an offer or recommendation to buy or sell a security. While information and sources are believed to be accurate, Allio Capital does not guarantee the accuracy or completeness of any information or source provided herein and is under no obligation to update this information.

Past performance is not a guarantee or a reliable indicator of future results. All investments contain risk and may lose value. Performance could be volatile; an investment in a fund or an account may lose money.

There is no guarantee that these investment strategies will work under all market conditions or are appropriate for all investors and each investor should evaluate their ability to invest long-term, especially during periods of downturn in the market.

This advertisement is provided by Allio Capital for informational purposes only and should not be considered investment advice, a recommendation, or a solicitation to buy or sell any securities. Investment decisions should be based on your specific financial situation and objectives, considering the risks and uncertainties associated with investing.

The views and forecasts expressed are those of Allio Capital and are subject to change without notice. Past performance is not indicative of future results, and investing involves risk, including the possible loss of principal. Market volatility, economic conditions, and changes in government policy may impact the accuracy of these forecasts and the performance of any investment.

Allio Capital utilizes proprietary technologies and methodologies, but no investment strategy can guarantee returns or eliminate risk. Investors should carefully consider their investment goals, risk tolerance, and financial circumstances before investing.

For more detailed information about our strategies and associated risks, please refer to the full disclosures available on our website or contact an Allio Capital advisor.

For informational purposes only; not personalized investment advice. All investments involve risk of loss. Past performance of any index or strategy is not indicative of future results. Any projections or forward-looking statements are hypothetical and not guaranteed. Allio is an SEC-registered investment adviser – see our Form ADV for details. No content should be construed as a recommendation to buy or sell any security.

What We Do

What We Say

Who We Are

Legal

Allio Advisors LLC ("Allio") is an SEC registered investment advisor. By using this website, you accept our Terms of Use and our Privacy Policy. Allio's investment advisory services are available only to residents of the United States. Nothing on this website should be considered an offer, recommendation, solicitation of an offer, or advice to buy or sell any security. The information provided herein is for informational and general educational purposes only and is not investment or financial advice. Additionally, Allio does not provide tax advice and investors are encouraged to consult with their tax advisor. By law, we must provide investment advice that is in the best interest of our client. Please refer to Allio's ADV Part 2A Brochure for important additional information. Please see our Customer Relationship Summary.

Online trading has inherent risk due to system response, execution price, speed, liquidity, market data and access times that may vary due to market conditions, system performance, market volatility, size and type of order and other factors. An investor should understand these and additional risks before trading. Any historical returns, expected returns, or probability projections are hypothetical in nature and may not reflect actual future performance. Past performance is no guarantee of future results.

Brokerage services will be provided to Allio clients through Allio Markets LLC, ("Allio Markets") SEC-registered broker-dealer and member FINRA/SIPC . Securities in your account protected up to $500,000. For details, please see www.sipc.org. Allio Advisors LLC and Allio Markets LLC are separate but affiliated companies.

Securities products are: Not FDIC insured · Not bank guaranteed · May lose value

Any investment , trade-related or brokerage questions shall be communicated to support@alliocapital.com

Please read Important Legal Disclosures

v1 01.20.2025

What We Do

What We Say

Who We Are

Legal

Allio Advisors LLC ("Allio") is an SEC registered investment advisor. By using this website, you accept our Terms of Use and our Privacy Policy. Allio's investment advisory services are available only to residents of the United States. Nothing on this website should be considered an offer, recommendation, solicitation of an offer, or advice to buy or sell any security. The information provided herein is for informational and general educational purposes only and is not investment or financial advice. Additionally, Allio does not provide tax advice and investors are encouraged to consult with their tax advisor. By law, we must provide investment advice that is in the best interest of our client. Please refer to Allio's ADV Part 2A Brochure for important additional information. Please see our Customer Relationship Summary.

Online trading has inherent risk due to system response, execution price, speed, liquidity, market data and access times that may vary due to market conditions, system performance, market volatility, size and type of order and other factors. An investor should understand these and additional risks before trading. Any historical returns, expected returns, or probability projections are hypothetical in nature and may not reflect actual future performance. Past performance is no guarantee of future results.

Brokerage services will be provided to Allio clients through Allio Markets LLC, ("Allio Markets") SEC-registered broker-dealer and member FINRA/SIPC . Securities in your account protected up to $500,000. For details, please see www.sipc.org. Allio Advisors LLC and Allio Markets LLC are separate but affiliated companies.

Securities products are: Not FDIC insured · Not bank guaranteed · May lose value

Any investment , trade-related or brokerage questions shall be communicated to support@alliocapital.com

Please read Important Legal Disclosures

v1 01.20.2025

What We Do

What We Say

Who We Are

Legal

Allio Advisors LLC ("Allio") is an SEC registered investment advisor. By using this website, you accept our Terms of Use and our Privacy Policy. Allio's investment advisory services are available only to residents of the United States. Nothing on this website should be considered an offer, recommendation, solicitation of an offer, or advice to buy or sell any security. The information provided herein is for informational and general educational purposes only and is not investment or financial advice. Additionally, Allio does not provide tax advice and investors are encouraged to consult with their tax advisor. By law, we must provide investment advice that is in the best interest of our client. Please refer to Allio's ADV Part 2A Brochure for important additional information. Please see our Customer Relationship Summary.

Online trading has inherent risk due to system response, execution price, speed, liquidity, market data and access times that may vary due to market conditions, system performance, market volatility, size and type of order and other factors. An investor should understand these and additional risks before trading. Any historical returns, expected returns, or probability projections are hypothetical in nature and may not reflect actual future performance. Past performance is no guarantee of future results.

Brokerage services will be provided to Allio clients through Allio Markets LLC, ("Allio Markets") SEC-registered broker-dealer and member FINRA/SIPC . Securities in your account protected up to $500,000. For details, please see www.sipc.org. Allio Advisors LLC and Allio Markets LLC are separate but affiliated companies.

Securities products are: Not FDIC insured · Not bank guaranteed · May lose value

Any investment , trade-related or brokerage questions shall be communicated to support@alliocapital.com

Please read Important Legal Disclosures

v1 01.20.2025